W

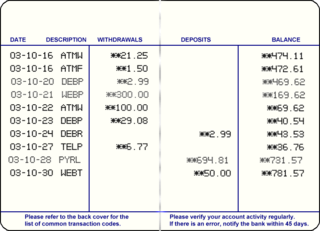

WA bank statement is an official summary of financial transactions occurring within a given period for each bank account held by a person or business with a financial institution. Such statements are prepared by the financial institution, are numbered and indicate the period covered by the statement, and may contain other relevant information for the account type, such as how much is payable by a certain date. The start date of the statement period is usually the day after the end of the previous statement period.

W

WA banknote—also called a bill, paper money, or simply a note—is a type of negotiable promissory note, made by a bank or other licensed authority, payable to the bearer on demand. Banknotes were originally issued by commercial banks, which were legally required to redeem the notes for legal tender when presented to the chief cashier of the originating bank. These commercial banknotes only traded at face value in the market served by the issuing bank. Commercial banknotes have primarily been replaced by national banknotes issued by central banks or monetary authorities.

W

WA cheque, or check, is a document that orders a bank to pay a specific amount of money from a person's account to the person in whose name the cheque has been issued. The person writing the cheque, known as the drawer, has a transaction banking account where the money is held. The drawer writes the various details including the monetary amount, date, and a payee on the cheque, and signs it, ordering their bank, known as the drawee, to pay that person or company the amount of money stated.

W

WA credit note or credit memo is a commercial document issued by a seller to a buyer. Credit notes act as a source document for the sales return journal. In other words the credit note is evidence of the reduction in sales. A credit memo, a contraction of the term "credit memorandum", is evidence of a reduction in the amount that a buyer owes a seller under the terms of an earlier invoice.

WA debit note or debit memorandum (memo) is a commercial document issued by a buyer to a seller as a means of formally requesting a credit note. Debit note acts as the Source document to the Purchase returns journal. In other words it is an evidence for the occurrence of a reduction in expenses. The seller might also issue a debit note instead of an invoice in order to adjust upwards the amount of an invoice already issued .

W

WA deposit slip is a form supplied by a bank for a depositor to fill out, designed to document in categories the items included in the deposit transaction. The categories include type of item, and if it is a cheque, where it is from such as a local bank or a state if the bank is not local. The teller keeps the deposit slip along with the deposit, and provides the depositor with a receipt. They are filled in a store and not a bank, so it is very convenient in paying. They also are a means of transport of money. Pay-in slips encourage the sorting of cash and coins, are filled in and signed by the person who deposited the money, and some tear off from a record that is also filled in by the depositor. Deposit slips are also called deposit tickets and come in a variety of designs. They are signed by the depositor if the depositor is cashing some of the accompanying check and depositing the rest.

W

WHundi/Hundee is a financial instrument that developed in Medieval India for use in trade and credit transactions. Hundis are used as a form of remittance instrument to transfer money from place to place, as a form of credit instrument or IOU to borrow money and as a bill of exchange in trade transactions. The Reserve Bank of India describes the Hundi as "an unconditional order in writing made by a person directing another to pay a certain sum of money to a person named in the order."

W

WA negotiable instrument is a document guaranteeing the payment of a specific amount of money, either on demand, or at a set time, whose payer is usually named on the document. More specifically, it is a document contemplated by or consisting of a contract, which promises the payment of money without condition, which may be paid either on demand or at a future date. The term has different meanings depending on the use of the term as it is used in the application of different laws, and depending in which country and context it is used.

W

WA passbook or bankbook is a paper book used to record bank or building society transactions on a deposit account.

W

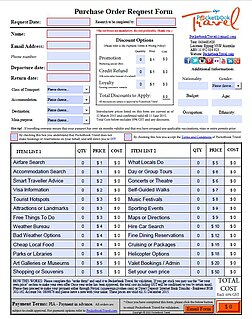

WA purchase order (PO) is a commercial document and first official offer issued by a buyer to a seller indicating types, quantities, and agreed prices for products or services. It is used to control the purchasing of products and services from external suppliers. Purchase orders can be an essential part of enterprise resource planning system orders.

W

WA receipt is a document acknowledging that a person has received money or property in payment following a sale or other transfer of goods or provision of a service. All receipts must have the date of purchase on them. If the recipient of the payment is legally required to collect sales tax or VAT from the customer, the amount would be added to the receipt and the collection would be deemed to have been on behalf of the relevant tax authority. In many countries, a retailer is required to include the sales tax or VAT in the displayed price of goods sold, from which the tax amount would be calculated at point of sale and remitted to the tax authorities in due course. Similarly, amounts may be deducted from amounts payable, as in the case of taxes withheld from wages. On the other hand, tips or other gratuities given by a customer, for example in a restaurant, would not form part of the payment amount or appear on the receipt.

WA receipt is a document acknowledging that a person has received money or property in payment following a sale or other transfer of goods or provision of a service. All receipts must have the date of purchase on them. If the recipient of the payment is legally required to collect sales tax or VAT from the customer, the amount would be added to the receipt and the collection would be deemed to have been on behalf of the relevant tax authority. In many countries, a retailer is required to include the sales tax or VAT in the displayed price of goods sold, from which the tax amount would be calculated at point of sale and remitted to the tax authorities in due course. Similarly, amounts may be deducted from amounts payable, as in the case of taxes withheld from wages. On the other hand, tips or other gratuities given by a customer, for example in a restaurant, would not form part of the payment amount or appear on the receipt.

W

WA voucher is a bond of the redeemable transaction type which is worth a certain monetary value and which may be spent only for specific reasons or on specific goods. Examples include housing, travel, and food vouchers. The term voucher is also a synonym for receipt and is often used to refer to receipts used as evidence of, for example, the declaration that a service has been performed or that an expenditure has been made. Voucher is a tourist guide for using services with a guarantee of payment by the agency.