W

WBank reserves are a commercial bank's cash holdings physically held by the bank, and deposits held in the bank's account with the central bank. Under the fractional-reserve banking system used in most countries, central banks typically set minimum reserve requirements that require commercial banks under its purview to hold cash or deposits at the central bank equivalent to at least a prescribed percentage of their liabilities, such as customer deposits. Such sums are usually termed required reserves, and any funds above the required amount are called excess reserves. These reserves are prescribed to ensure that, in the normal events, there is sufficient liquidity in the banking system to provide funds to bank customers wishing to withdraw cash. Even when there are no reserve requirements, banks often as a matter of prudent management hold reserves in case of unexpected events, such as unusually large net withdrawals by customers or bank runs. In general, banks do not earn any interest on their reserves. Funds in banks that are not retained as a reserve are available to be lent, at interest.

W

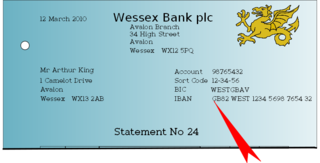

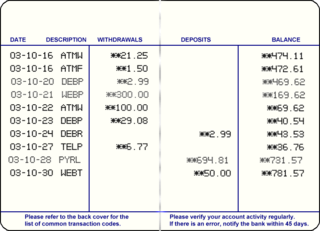

WA bank statement is an official summary of financial transactions occurring within a given period for each bank account held by a person or business with a financial institution. Such statements are prepared by the financial institution, are numbered and indicate the period covered by the statement, and may contain other relevant information for the account type, such as how much is payable by a certain date. The start date of the statement period is usually the day after the end of the previous statement period.

W

WA banking agent is a retail or postal outlet contracted by a financial institution or a mobile network operator to process clients’ transactions. Rather than a branch teller, it is the owner or an employee of the retail outlet who conducts the transaction and lets clients deposit, withdraw, transfer funds, pay their bills, inquire about an account balance, or receive government benefits or a direct deposit from their employer. Banking agents can be pharmacies, supermarkets, convenience stores, lottery outlets, post offices, and more.

W

WA branch, banking center or financial center is a retail location where a bank, credit union, or other financial institution offers a wide array of face-to-face and automated services to its customers.

WA central bank, reserve bank, or monetary authority is an institution that manages the currency and monetary policy of a state or formal monetary union, and oversees their commercial banking system. In contrast to a commercial bank, a central bank possesses a monopoly on increasing the monetary base. Most central banks also have supervisory and regulatory powers to ensure the stability of member institutions, to prevent bank runs, and to discourage reckless or fraudulent behavior by member banks.

W

WA cheque, or check, is a document that orders a bank to pay a specific amount of money from a person's account to the person in whose name the cheque has been issued. The person writing the cheque, known as the drawer, has a transaction banking account where the money is held. The drawer writes the various details including the monetary amount, date, and a payee on the cheque, and signs it, ordering their bank, known as the drawee, to pay that person or company the amount of money stated.

W

WCheque truncation is a cheque clearance system that involves the digitalisation of a physical paper cheque into a substitute electronic form for transmission to the paying bank. The process of cheque clearance, involving data matching and verification, is done using digital images instead of paper copies.

W

WA deposit slip is a form supplied by a bank for a depositor to fill out, designed to document in categories the items included in the deposit transaction. The categories include type of item, and if it is a cheque, where it is from such as a local bank or a state if the bank is not local. The teller keeps the deposit slip along with the deposit, and provides the depositor with a receipt. They are filled in a store and not a bank, so it is very convenient in paying. They also are a means of transport of money. Pay-in slips encourage the sorting of cash and coins, are filled in and signed by the person who deposited the money, and some tear off from a record that is also filled in by the depositor. Deposit slips are also called deposit tickets and come in a variety of designs. They are signed by the depositor if the depositor is cashing some of the accompanying check and depositing the rest.

The Eurocheque was a type of cheque used in Europe that was accepted across national borders and which could be written in a variety of currencies.

WFree banking is a monetary arrangement where banks are free to issue their own paper currency (banknotes) while also subject to no special regulations beyond those applicable to most enterprises.

W

WIn finance, a high-yield bond is a bond that is rated below investment grade by credit rating agencies. These bonds have a higher risk of default or other adverse credit events, but offer higher yields than investment-grade bonds in order to compensate for the increased risk.

W

WIjarah,, is a term of fiqh and product in Islamic banking and finance. In traditional fiqh, it means a contract for the hiring of persons or renting/leasing of the services or the “usufruct” of a property, generally for a fixed period and price. In hiring, the employer is called musta’jir, while the employee is called ajir. Ijarah need not lead to purchase. In conventional leasing an "operating lease" does not end in a change of ownership, nor does the type of ijarah known as al-ijarah (tashghiliyah).

W

WThe International Bank Account Number (IBAN) is an internationally agreed system of identifying bank accounts across national borders to facilitate the communication and processing of cross border transactions with a reduced risk of transcription errors. An IBAN uniquely identifies the account of a customer at a financial institution. It was originally adopted by the European Committee for Banking Standards (ECBS) and later as an international standard under ISO 13616:1997. The current standard is ISO 13616:2020, which indicates SWIFT as the formal registrar. Initially developed to facilitate payments within the European Union, it has been implemented by most European countries and numerous countries in other parts of the world, mainly in the Middle East and the Caribbean. As of May 2020, 77 countries were using the IBAN numbering system.

W

WIn finance, a loan is the lending of money by one or more individuals, organizations, or other entities to other individuals, organizations etc. The recipient incurs a debt and is usually liable to pay interest on that debt until it is repaid as well as to repay the principal amount borrowed.

W

WAn overdraft occurs when money is withdrawn in excess of what is on the current account. In this situation the account is said to be "overdrawn". If there is a prior agreement with the account provider for an overdraft, and the amount overdrawn is within the authorized overdraft limit, then interest is normally charged at the agreed rate. If the negative balance exceeds the agreed terms, then additional fees may be charged and higher interest rates may apply.

W

WA passbook or bankbook is a paper book used to record bank or building society transactions on a deposit account.

W

WA personal identification number (PIN), or sometimes redundantly a PIN number, is a numeric passcode used in the process of authenticating a user accessing a system.

W

WIn accounting, reconciliation is the process of ensuring that two sets of records are in agreement. Reconciliation is used to ensure that the money leaving an account matches the actual money spent. This is done by making sure the balances match at the end of a particular accounting period.

W

WA safe deposit box, also known as a safety deposit box, is an individually secured container, usually held within a larger safe or bank vault. Safe deposit boxes are generally located in banks, post offices or other institutions. Safe deposit boxes are used to store valuable possessions, such as gemstones, precious metals, currency, marketable securities, luxury goods, important documents, or computer data, which need protection from theft, fire, flood, tampering, or other perils. In the United States, neither banks nor the FDIC insure the contents. An individual can purchase separate insurance for the safe deposit box in order to cover e.g. theft, fire, flooding or terrorist attacks.

W

WThe Islamic banking and finance movement that developed in the late 20th century as part of the revival of Islamic identity sought to create an alternative to conventional banking that complied with sharia (Islamic) law. Following sharia it banned from its practices riba (usury) – which it defined as any interest paid on all loans of money – and involvement in haram (forbidden) goods or services such as pork or alcohol. It also forbids gambling (maisir) and excessive risk.

WA cheque, or check, is a document that orders a bank to pay a specific amount of money from a person's account to the person in whose name the cheque has been issued. The person writing the cheque, known as the drawer, has a transaction banking account where the money is held. The drawer writes the various details including the monetary amount, date, and a payee on the cheque, and signs it, ordering their bank, known as the drawee, to pay that person or company the amount of money stated.

WThe substitute check is a negotiable instrument that represents the digital reproduction of an original paper check. As a negotiable payment instrument in the United States, a substitute check maintains the status of a "legal check" in lieu of the original paper check as authorized by the Check Clearing for the 21st Century Act. Instead of presenting the original paper checks, financial institutions and payment processing centers transmit data from a substitute check electronically through either the settlement process, the United States Federal Reserve System, or by clearing the deposit based on a private agreement between member financial institutions of a clearinghouse that operates under the Uniform Commercial Code (UCC).

WWholesale funding is a method that banks use in addition to core demand deposits to finance operations and manage risk. Wholesale funding sources include, but are not limited to, Federal funds, public funds, U.S. Federal Home Loan Bank advances, the U.S. Federal Reserve's primary credit program, foreign deposits, brokered deposits, and deposits obtained through the Internet or CD listing services.